All Categories

Featured

Table of Contents

When life quits, the bereaved have no choice however to maintain moving. Virtually instantly, households must handle the overwhelming logistics of fatality adhering to the loss of a loved one. This can include paying expenses, splitting possessions, and handling the interment or cremation. However while fatality, like taxes, is inescapable, it does not have to burden those left behind.

Furthermore, a complete survivor benefit is commonly offered for unintended fatality. A customized death advantage returns premium commonly at 10% passion if death happens in the very first 2 years and includes the most loosened up underwriting. The full fatality advantage is frequently given for unintended death. The majority of sales are carried out in person, and the industry fad is to approve an electronic or voice signature, with point-of-sale choices collected and videotaped by means of a laptop or tablet computer.

To finance this organization, firms rely upon personal wellness interviews or third-party information such as prescription backgrounds, scams checks, or car records. Underwriting tele-interviews and prescription backgrounds can typically be made use of to help the agent finish the application procedure. Historically business count on telephone meetings to validate or validate disclosure, yet more recently to enhance client experience, companies are counting on the third-party information indicated over and giving split second choices at the factor of sale without the meeting.

Senior Final Expense Insurance Program

What is last cost insurance, and is it always the finest path onward? Listed below, we take an appearance at exactly how final expenditure insurance works and variables to think about prior to you purchase it.

However while it is called a plan to cover final expenses, beneficiaries that receive the death benefit are not called for to use it to spend for last costs they can utilize it for any kind of function they such as. That's because last expense insurance coverage truly falls into the classification of changed entire life insurance policy or simplified problem life insurance policy, which are typically whole life policies with smaller survivor benefit, usually in between $2,000 and $20,000.

Our opinions are our own. Funeral insurance is a life insurance policy that covers end-of-life costs.

What's The Difference Between Life Insurance And Burial Insurance

Burial insurance requires no clinical exam, making it easily accessible to those with medical problems. The loss of a loved one is emotional and stressful. Making funeral preparations and finding a method to spend for them while regreting adds another layer of anxiety. This is where having interment insurance, likewise referred to as last expenditure insurance, can be found in helpful.

Streamlined issue life insurance coverage calls for a health analysis. If your health status disqualifies you from traditional life insurance policy, funeral insurance may be an option. Along with fewer health and wellness examination requirements, burial insurance coverage has a quick turnaround time for authorizations. You can obtain protection within days or even the very same day you apply.

Compare economical life insurance policy alternatives with Policygenius. Term and irreversible life insurance, burial insurance can be found in numerous kinds. Have a look at your insurance coverage alternatives for funeral expenditures. Guaranteed-issue life insurance policy has no wellness demands and offers fast authorization for protection, which can be practical if you have severe, incurable, or several health problems.

Covering Funeral Costs

Simplified issue life insurance policy does not require a clinical test, but it does call for a health survey. This policy is best for those with light to modest health and wellness problems, like high blood pressure, diabetes mellitus, or asthma. If you do not want a medical exam yet can get a simplified issue plan, it is typically a far better bargain than a guaranteed problem policy because you can get more insurance coverage for a more affordable premium.

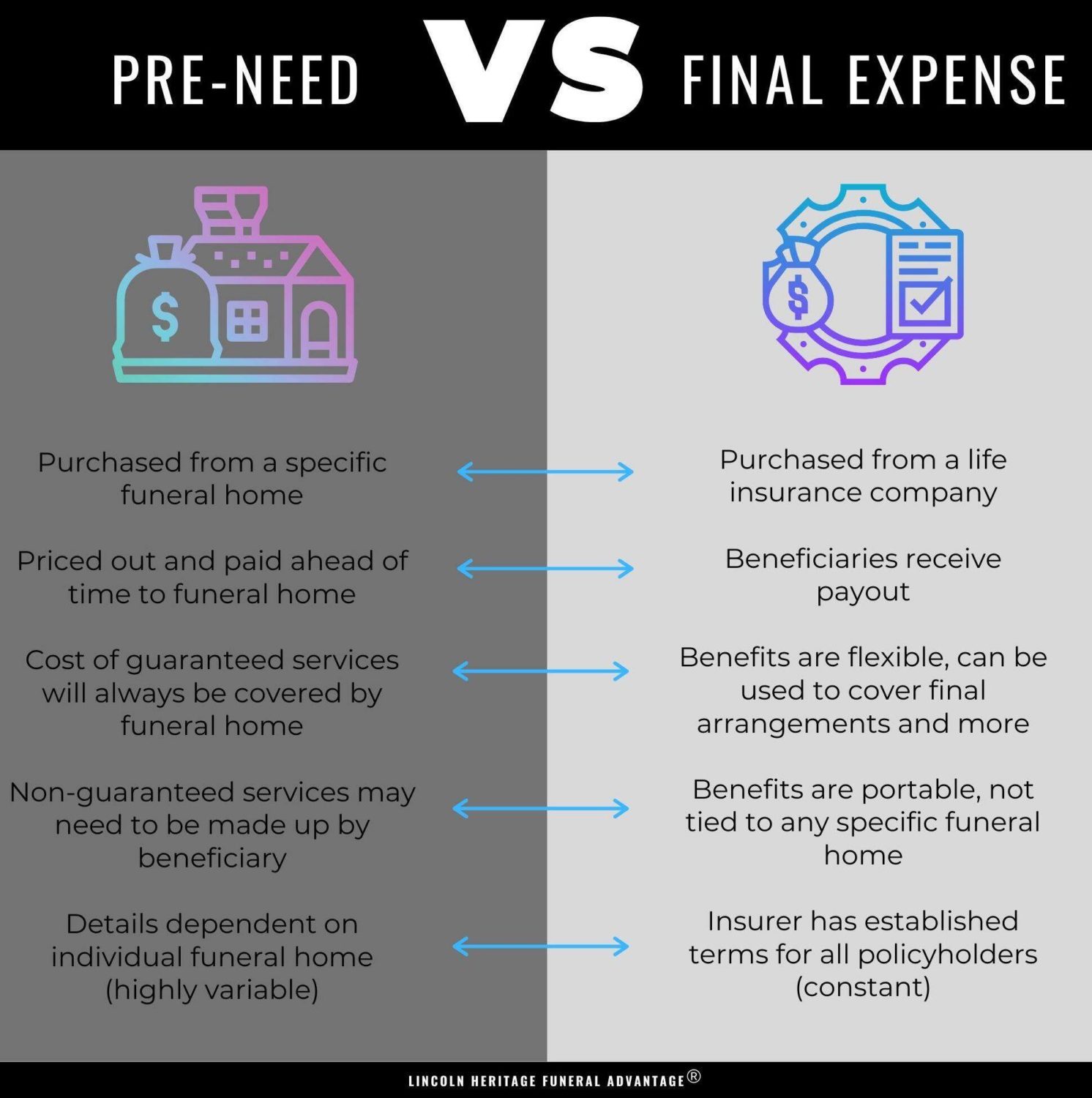

Pre-need insurance policy is dangerous because the recipient is the funeral home and coverage is details to the selected funeral chapel. Must the funeral home fail or you relocate out of state, you may not have coverage, and that beats the function of pre-planning. Furthermore, according to the AARP, the Funeral Consumers Alliance (FCA) discourages buying pre-need.

Those are essentially interment insurance coverage plans. For guaranteed life insurance coverage, costs estimations depend on your age, sex, where you live, and insurance coverage quantity.

Funeral insurance provides a simplified application for end-of-life coverage. A lot of insurance business need you to talk to an insurance agent to apply for a policy and acquire a quote.

The goal of living insurance policy is to relieve the burden on your enjoyed ones after your loss. If you have a supplementary funeral service policy, your enjoyed ones can use the funeral policy to deal with final costs and obtain an immediate disbursement from your life insurance policy to handle the home loan and education and learning prices.

Individuals who are middle-aged or older with medical problems may take into consideration interment insurance, as they could not get approved for typical plans with stricter approval standards. In addition, funeral insurance policy can be useful to those without considerable cost savings or typical life insurance policy coverage. Interment insurance policy varies from various other kinds of insurance coverage in that it offers a reduced survivor benefit, generally only adequate to cover expenses for a funeral service and various other linked costs.

Life Insurance Final Expense

News & World Record. ExperienceAlani has evaluated life insurance coverage and animal insurance policy firms and has actually composed numerous explainers on traveling insurance coverage, credit rating, financial debt, and home insurance policy. She is enthusiastic regarding debunking the intricacies of insurance policy and other personal financing subjects to make sure that readers have the information they require to make the very best cash decisions.

Last expenditure life insurance policy has a number of benefits. Last expenditure insurance is typically suggested for seniors that might not qualify for traditional life insurance policy due to their age.

Additionally, last expense insurance is helpful for people that wish to pay for their own funeral. Burial and cremation services can be pricey, so final expense insurance policy gives peace of mind knowing that your liked ones will not need to utilize their financial savings to pay for your end-of-life plans. Nonetheless, last expenditure insurance coverage is not the best product for everybody.

Guaranteed Whole Life Final Expense Insurance

You can look into Ethos' overview to insurance coverage at various ages if you need aid deciding what sort of life insurance is best for your phase in life. Obtaining entire life insurance policy via Principles is fast and very easy. Protection is offered for elders between the ages of 66-85, and there's no medical examination called for.

Based on your actions, you'll see your estimated price and the quantity of protection you qualify for (in between $1,000-$30,000). You can purchase a plan online, and your coverage begins immediately after paying the first premium. Your price never ever changes, and you are covered for your entire lifetime, if you continue making the regular monthly repayments.

Eventually, most of us have to believe concerning how we'll pay for a loved one's, or perhaps our very own, end-of-life costs. When you offer final expense insurance policy, you can give your clients with the satisfaction that features recognizing they and their families are planned for the future. You can additionally get an opportunity to maximize your publication of service and produce a brand-new revenue stream! Ready to find out every little thing you require to know to start offering last cost insurance policy effectively? No one suches as to consider their own death, yet the truth of the matter is funerals and interments aren't inexpensive.

Furthermore, clients for this kind of strategy could have severe legal or criminal backgrounds. It is essential to note that different carriers provide a series of problem ages on their ensured problem policies as low as age 40 or as high as age 80. Some will certainly additionally supply higher face worths, as much as $40,000, and others will enable much better survivor benefit conditions by boosting the rate of interest with the return of costs or minimizing the number of years till a full survivor benefit is readily available.

{kind=link}

Latest Posts

Which Of The Following Statements Regarding Term Life Insurance Is Incorrect?

Face Value Of Term Life Insurance

Family Income Benefit Term Life Insurance